Insurance panel status providers get reimbursed, how patients receive care, and how claims go through the revenue cycle. In 2026, the problem is getting worse. About 35.5 million Medicare beneficiaries are enrolled in Medicare Advantage plans, and managed care currently serves more than half of all Medicare patients. At the same time, insurers will reduce available Medicare Advantage plans by approximately 9% between 2025 and 2026, tightening network participation restrictions and increasing panel closures.

For providers, billers, and coders, panel status is no longer just a technical detail. Closed panels slow credentialing, reduce patient volume, and raise out-of-network billing risks. In 2026, approximately 10% of Medicare Advantage subscribers were affected by plan terminations or service-area exits, necessitating that providers recheck participation status midyear. When panels status is not confirmed promptly, these changes will result in more denied claims, patient uncertainty, and unpaid balances.

This blog explains insurance panel status in practical terms. It breaks down open versus closed panels, explains how payers decide network limits, and outlines the operational impact on billing, coding, and compliance teams. Each section focuses on real risks and workable steps so healthcare professionals can protect access, reimbursement, and regulatory alignment in a tightening payer environment.

Insurance panel status

Insurance panel status defines whether a healthcare provider is permitted to deliver covered services as an in-network participant for a specific payer. It directly affects reimbursement eligibility, patient cost-sharing, and claim processing.

What is the insurance panel status?

Insurance panel status refers to a payer’s determination of whether a provider may participate in its network. Approval requires two separate steps:

- Credentialing approval, which validates licensure, training, and compliance

- Panel acceptance, which determines if the payer is adding providers in that specialty and location

A provider may be fully credentialed yet still denied network participation due to panel restrictions. This distinction is often misunderstood and leads to billing errors.

Panel status is payer-specific. A provider may be in-network with one commercial payer and excluded from another, even within the same geographic area.

Why payers control panel status

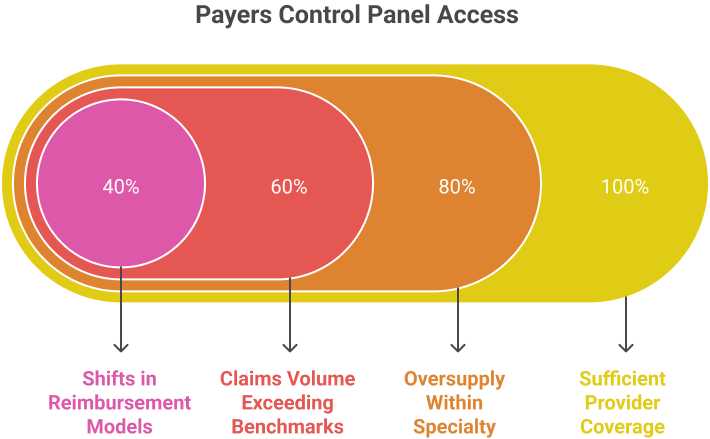

Payers regulate panel access to manage cost, utilization, and network balance. Closed panels typically result from:

- Sufficient provider coverage in a service area

- Oversupply within a specialty

- Claims volume exceeding payer benchmarks

- Shifts in reimbursement models tied to outcomes

For Medicare Advantage and Medicaid managed care plans, panel limits also align with government contracts and risk adjustment models.

From a billing and compliance standpoint, panel status determines:

- Whether claims are processed as in-network or out-of-network

- Patient liability exposure

- Authorization requirements

- Audit vulnerability

Insurance panels status explained: open vs closed panels for healthcare providers.

Closed panels limit in-network participation, often forcing providers to bill out-of-network. Understanding panel status early helps medical billers, coders, and practice managers reduce claim denials and maintain compliance.

What does open insurance panels for doctors mean

An open insurance panel allows new providers to apply for in-network status. Providers on open panels can:

- Submit claims as in-network providers.

- Receive standard reimbursement rates set by the payer.

- Access referrals from existing in-network providers.

What does insurance panels closed mean

A closed panel occurs when a payer stops accepting new providers in-network. Providers excluded from closed panels may:

- Only see patients out-of-network.

- Face reduced reimbursement rates or patient balance responsibilities.

- Encounter delays in credentialing and network integration.

Insurance network participation rules

Understanding insurance network participation rules helps providers manage credentialing, panel access, and reimbursements. This section explains how contracting and panel status affect claims and revenue cycle management.

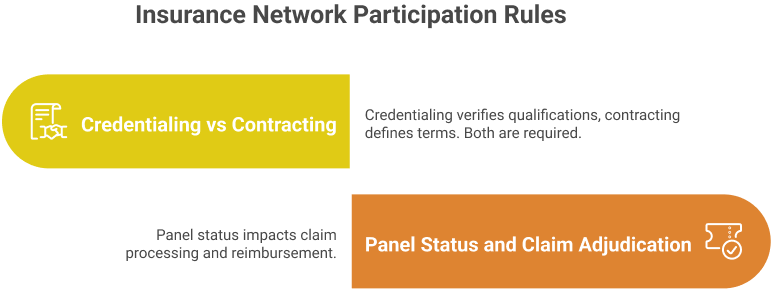

Credentialing vs contracting

Credentialing verifies a provider’s qualifications, licensure, and experience before they can join a payer’s network. Contracting is the agreement that defines reimbursement rates, billing procedures, and obligations. Both are required for in-network participation. Providers should ensure credentialing documents are current and contracts are reviewed by compliance or legal experts to avoid delays.

Key points:

- Credentialing approvals can take 90–180 days in 2026.

- Contracting sets in-network reimbursement rates and claim submission rules.

- Missing or outdated documents can result in delayed panel acceptance.

Panel status and claim adjudication

Panel status directly impacts how claims are processed. In-network providers on open panels receive standard reimbursement. Closed panels prevent new in-network billing, requiring out-of-network claims or single-case agreements.

Important considerations:

- Out-of-network claims may have reduced reimbursement or higher patient responsibility.

- Insurers may reopen panels periodically; tracking payer updates quarterly is critical.

- Properly documenting panel status in the practice management system prevents claim denials.

How to get on a closed insurance panel

Gaining access to closed insurance panels requires understanding reapplication schedules and providing data-backed appeals. This section explains actionable steps for providers to increase the chances of approval.

Reapplication timelines

Closed panels are not always permanent. Insurers periodically reassess network capacity. Providers should:

- Track payer policies; many reevaluate panels every 3–12 months in 2026.

- Keep credentials updated to avoid delays in reapplication.

- Submit applications promptly once panels reopen to secure consideration.

Appeals with data support

Appeals can influence insurers to grant access even on closed panels. A strong appeal uses facts and measurable data:

- Highlight patient demand in the coverage area.

- Show specialized services, certifications, or equipment that differentiates your practice.

- Include referrals from in-network physicians or hospital affiliations.

- Present patient outcome metrics or cost-saving examples where possible.

Single-case agreements

Single-case agreements allow a provider to treat a patient under in-network terms, even if the panel is closed. Key points:

- Request agreements for patients with urgent or specialized care needs unavailable in-network.

- Provide documentation showing patient benefit and cost efficiency for the payer.

- Use the agreement to demonstrate your value and improve chances of full panel acceptance.

- Track outcomes and patient satisfaction to support future applications.

Referral-based justification

Providers can leverage referrals to support panel inclusion:

- Compile evidence from in-network physicians or hospital groups recommending your services.

- Demonstrate that out-of-network restrictions are impacting patient access.

- Highlight specialty skills or certifications that fill gaps in the network.

- Present patient volume data and regional service shortages to strengthen the case.

Revenue cycle impact of insurance panel status

Insurance panel status directly affects provider revenue, claim processing, and patient satisfaction. Understanding how open or closed panels influence billing and reimbursement is critical for healthcare providers and billing teams.

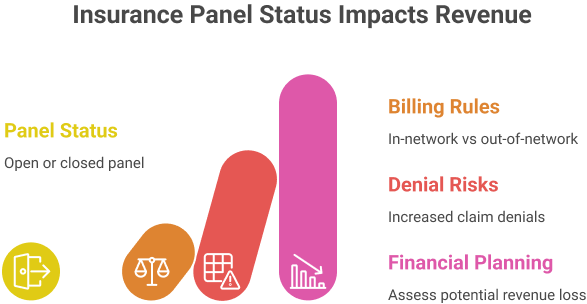

In-network vs out-of-network billing rules

Panel status determines whether a provider can bill in-network or must submit out-of-network claims:

In-network: Providers must follow payer fee schedules, pre-authorization rules, and claim submission requirements. Payment is usually faster, with predictable reimbursement rates.

Out-of-network: Claims may be partially reimbursed or denied, depending on patient coverage. Providers should verify out-of-network benefits, deductibles, and patient responsibility.

Financial planning: Practices should assess patient demographics and plan types to determine potential revenue loss if denied panel access.

Coding, authorization, and denial risks

Panel status influences claim accuracy, authorization, and denial rates:

- Providers on closed panels may face increased claim denials if services are billed out-of-network.

- Authorization requirements may differ between in-network and out-of-network claims, affecting workflow.

- Proper CPT, HCPCS, and ICD-10 coding is essential to avoid delayed payments or compliance issues.

- Implementing denial tracking and appeals processes helps mitigate revenue loss from panel limitations.

Compliance risks tied to panel status

Insurance panel status is not only a financial concern, but it also carries legal and regulatory implications. Providers must understand how open or closed panels affect compliance and billing integrity.

False claims exposure

Submitting claims while misrepresenting network status can trigger serious legal issues:

- Billing an insurer as in-network when the provider is actually out-of-network may constitute a false claim.

- Violations can lead to civil penalties under the False Claims Act (FCA) and state-level equivalents.

- Practices should ensure billing teams verify panel status before claim submission.

Audit and recoupment risk

Closed panel participation increases the likelihood of audits and payment recoupment:

- Insurers may review claims for compliance with panel agreements.

- Out-of-network billing errors can result in retroactive denials and repayment demands.

- Proper documentation of patient eligibility, prior authorizations, and provider credentials is critical to defend against recoupment.

Conclusion

Insurance panel status now directly affects reimbursement accuracy, patient access, and claim resolution. As payer networks tighten, failure to verify panel participation exposes providers to denials, payment gaps, and compliance review.

Clear panel tracking, disciplined reapplication planning, and correct billing pathways reduce financial leakage. Practices that align credentialing, contracting, and audit controls are better positioned to sustain revenue and care access under restricted payer networks.

FAQs

What is insurance panel status in healthcare billing?

Insurance panel status shows whether a provider is approved as in-network for a payer. It controls reimbursement rates, patient cost-sharing, and claim processing rules.

What does it mean when an insurance panel is closed?

A closed panel means the payer is not adding new in-network providers. Services may require out-of-network billing or single-case agreements.

Can a provider be credentialed but still denied panel access?

Yes. Credentialing confirms qualifications, but panel acceptance depends on payer network limits and regional coverage needs.

How does insurance panel status affect claim denials?

Incorrect panel status leads to out-of-network processing or rejections. This increases denials, delayed payments, and patient balance exposure.

How can providers access closed insurance panels?

Providers may reapply during review cycles, submit data-based appeals, request single-case agreements, or use referral-based justification.